Form 941 Instructions

for 2023

Step by Step instructions to fill out the Form 941

E-File 941 Now!Form 941 Q2 Deadline is on

August 02, 2021

E-file 3rd quarter Form 941 for the lowest

price ($5.95)

with ExpressEfile. E-file Now

IRS Form 941 Filing Instructions

Updated on October 23, 2023 - 10:30 AM by Admin, ExpressEfile

Form 941 is an employer’s quarterly tax form that is filed by employers to report federal income tax withholdings from employees. The calculation of these taxes and filing of this return can be quite confusing. You can take a look at these line-by-line instructions, to get a better understanding of how to file your

Form 941 return.

In this article, we cover the following topics:

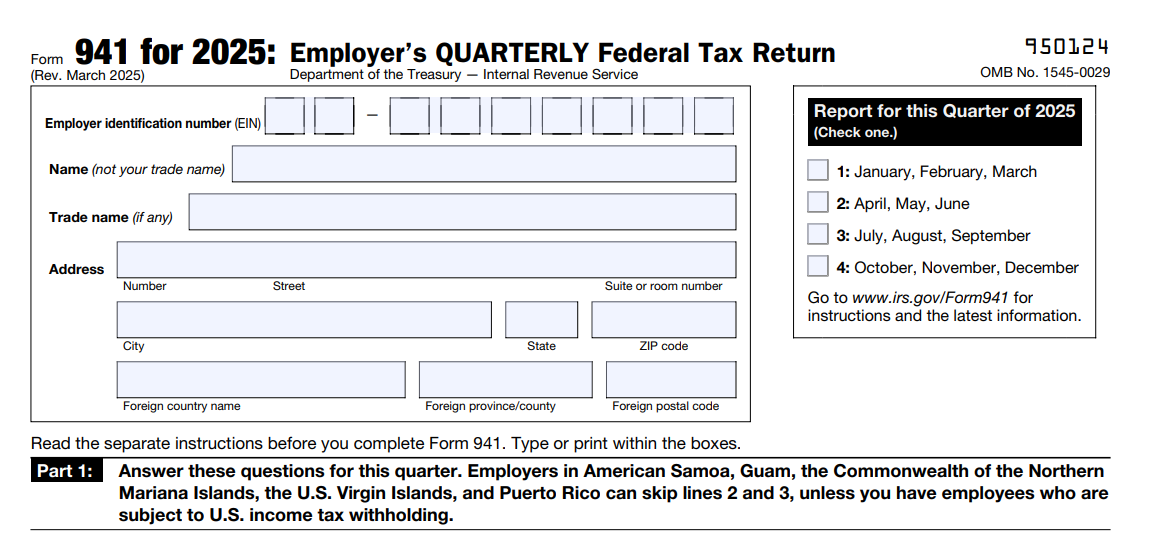

1. Provide Business Information

The first step in filing your Form 941 return is to enter basic information about

your business.

Employer Identification Number (EIN): Enter your business’s 9-digit EIN. It’s mandatory to have an EIN to file Form 941. What if you don’t have an EIN?

Learn more.

Name: Enter the business name associated with the EIN. Please make sure you’re not entering your trade name or DBA name.

Trade name: Enter the other name under which you’re operating your business

(if any)

Business address: Enter your primary business address. The IRS will use this address to send important communication.

Choose the correct quarter for which you are filing your Form 941 return. For example, if you’re filing for the Third quarter, check the box next to

“July, August, September”.

2. Part 1 - Wages, COVID-19 Changes, Credits

This part of the return involves reporting information about employees, their wages, and the federal income taxes withheld from their paychecks during

the quarter.

-

Line 1: Number of employees who received wages, tips, or other compensation for the pay period including: June 12 (Quarter 2), Sept. 12 (Quarter 3), or Dec. 12 (Quarter 4)

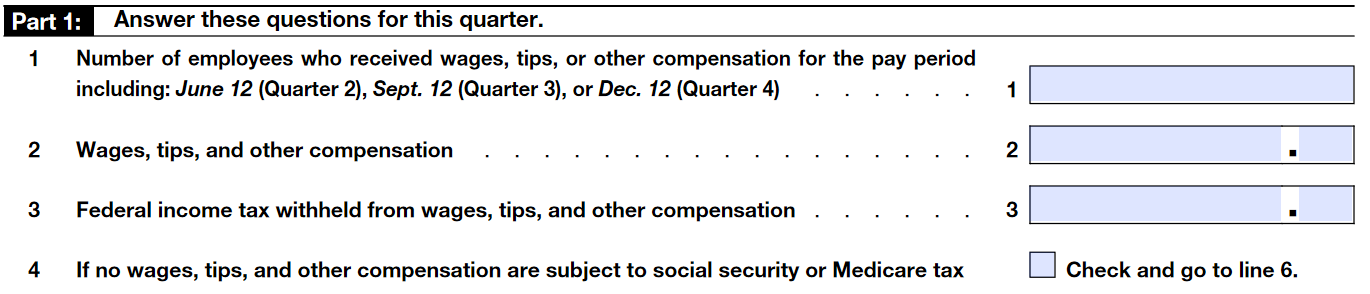

Enter the number of employees, who received wages, tips, or other payments in

the quarter. -

Line 2: Wages, tips, and other compensation

Enter the total amount of wages, tips, and other payments paid to all the employees in

the quarter. -

Line 3: Federal income tax withheld from wages, tips, and other compensation

Enter the total amount of federal tax withheld from all the employees’ paychecks.

-

Line 4: Checkbox

If the wages aren’t subjected to any social security or Medicare taxes, check this box. Skip this line if these taxes apply.

-

Line 5a, 5a(i) and 5a(ii):

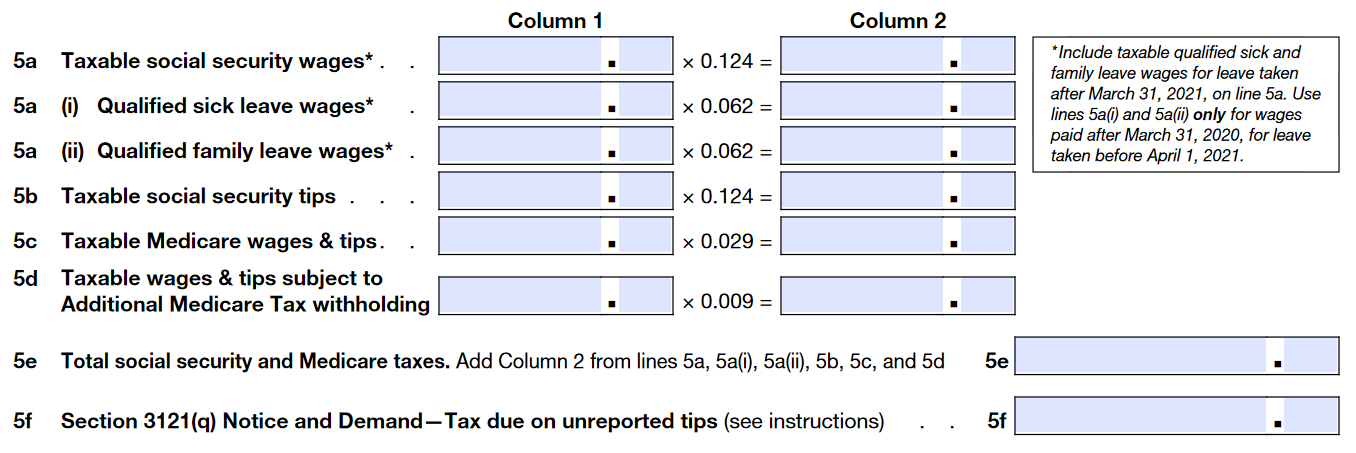

Report the total wages, including qualified sick and family leave wages, paid to your employees after March 31, 2020. Also report qualified taxable sick and family leave wages for leave taken before April 1, 2021.

-

Line 5b: Taxable social security tips

Enter the total amount of taxable security tips received by all employees (excluding pretax amounts).

-

Line 5c: Taxable Medicare wages & tips

Enter the total amount of taxable wages, and tips, that are subject to Medicare tax (excluding pretax amounts).

-

Line 5d: Taxable wages & tips subject to Additional Medicare Tax withholding

Enter the total amount of taxable wages & tips subject to Additional Medicare Tax withholding (excluding pretax amounts).

Additional Medicare Tax: If an employee’s wages exceed a certain threshold limit, the employer has to withhold additional Medicare tax from the employee’s pay. The threshold limit is based on the employee’s filing status, and the rate is 0.9%. Below is the threshold limit based on filing status:

Filing Status Threshold Limit Married filing jointly $250,000 Married filing separately $125,000 Single $200,000 Head of household $200,000 Qualifying widow(er) with dependent child $200,000 -

Line 5e: Total social security and Medicare taxes

This line should contain the sum of values from column 2 of lines 5a, 5b, 5c, and 5d.

-

Line 5f: Section 3121(q) Notice and Demand—Tax due on unreported tips

Enter the total tax due received from Section 3121(q) Notice and Demand.

Section 3121(q) Notice and Demand - This is issued by the IRS to advise the employers to report the tips that the employees haven’t reported. The employers aren’t required to report this information until they receive

this notice.

-

Line 6: Total taxes before adjustments

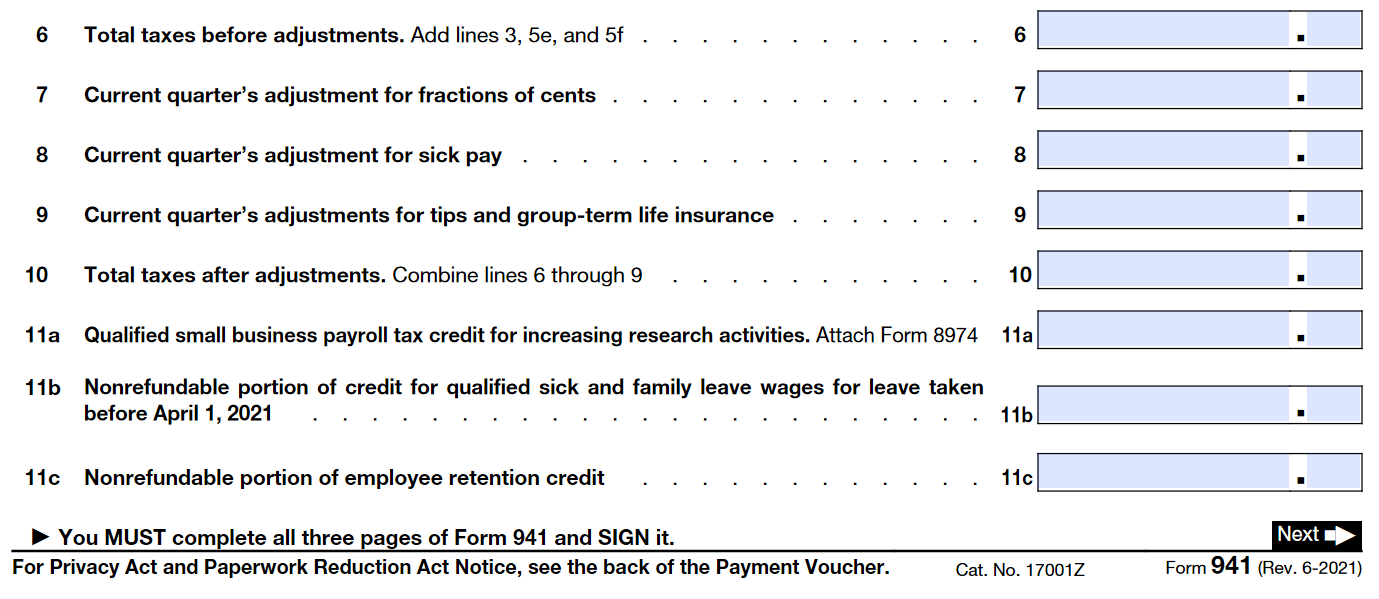

The value entered in this line should be a sum of lines 3, 5e, and 5f.

-

Line 7: Current quarter’s adjustment for fractions of cents

Enter the adjustment for a fraction of cents.

Fractions-of-cents: While running payroll, social security and Medicare taxes are calculated. If the calculated tax values are in fractions-of-cents, the amount will be rounded to the nearest cent. If you notice a small difference between your total taxes after adjustments and credits and total deposits, you have to report in this line.

-

Line 8: Current quarter’s adjustment

for sick payEnter the adjustment for sick pay.

If your third-party payer of sick pay transfers the liability for the employer share of Social Security and Medicare taxes to you, enter a negative adjustment on line 8 for the amount the third-party payer withheld

and deposited. -

Line 9: Current quarter’s adjustments for tips and group-term

life insuranceEnter the adjustments for tips and group-terms

life insurance.Enter a negative adjustment for any uncollected employee share of social security and Medicare taxes on tips, and the uncollected employee share of social security and Medicare taxes on group-term life insurance premiums paid for former employees.

-

Line 10: Total taxes after adjustments

Enter the total tax after the adjustments. Add the values from lines 6, 7, 8, and 9.

-

Line 11a: Qualified small business payroll tax credit for increasing

research activitiesEnter the amount calculated in Form 8974.

Form 8874 - This form is used to calculate the amount of credit that can be claimed for the increasing research activities.

-

Line 11b:

Enter the non refundable portion of qualified sick and family leave wages for leave taken before April 1, 2021. You can calculate these credits on Worksheet 1.

-

Line 11c: Nonrefundable portion of employee retention credit from

Worksheet 1 (Not part of the original form. Included due to COVID-19 changes)Use Worksheet 1 to calculate the amount of the employee retention credit for which it is eligible with respect to the quarter.

-

Line 11d:

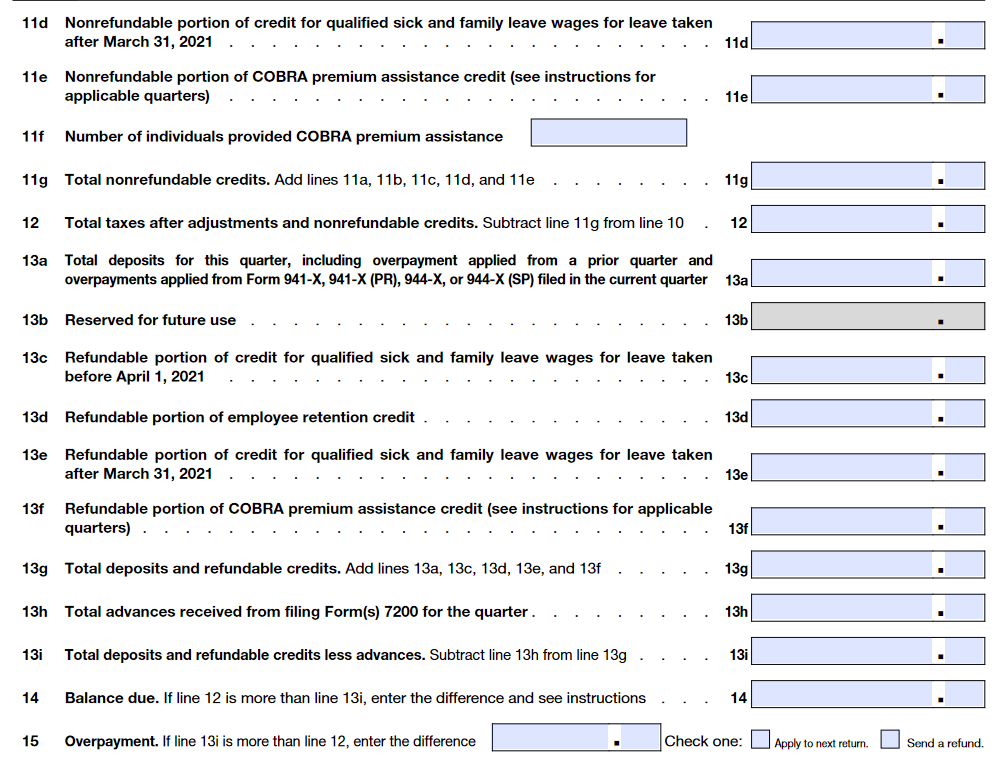

Enter the non refundable portion of credits for qualified sick and family leave wages for leave taken before March 31, 2021. These credits can be calculated using Worksheet 3.

-

Line 11e:

Enter the non refundable portion of COBRA premium assistance that you provided for the quarter. These credits can be calculated using Worksheet 5.

-

Line 11f:

Report the number of individuals who were provided COBRA premium assistance

for the quarter. -

Line 11g:

To report total nonrefundable credits, add together lines 11a, 11b, 11c, 11d, and 11e, and enter the total on line 11g.

-

Line 12: Total taxes after adjustments and nonrefundable credits

Enter the total taxes after the adjustments and credits. Subtract line 11d from line 10.

-

Line 13a: Total deposits for this quarter, including overpayment applied from a prior quarter and overpayments applied from Form 941-X, 941-X (PR), 944-X, or 944-X (SP) filed in the current quarter

Enter the total amount of deposits for the quarter. This should include overpayment applied from previous quarters and Form 941-X for the

current quarter. -

Line 13b: Reserved for future use

No need to report anything in this line.

-

Line 13c:

To report on the refundable portion of credits for qualified sick and family leave wages for leave taken before April 1, 2021, enter the amount from Worksheet 1.

-

Line 13d: Refundable portion of employee retention credit from Worksheet 4 (Not part of the original form. Included due to COVID-19 changes)

After determining the nonrefundable employee retention credit using Worksheet 4, subtract the amount of the non refundable portion from the total amount of the credit to determine the amount of the refundable portion. Enter the refundable portion of the credit identified in Line 3k of the worksheet in

Line 13d. -

Line 13e:

Enter the refundable portion of credits for qualified sick and family leave wages for leave taken after March 31, 2021 from Worksheet 3.

-

Line 13f:

Enter the refundable portion of COBRA premium assistance credit from Worksheet 1.

-

Line 13g:

To report the total deposits and refundable credits, add lines 13a, 13c, 13d, 13e, and 13f and enter the total on line 13g.

-

Line 13h:

Enter the total advances that you received by filing Form 7200 for the quarter.

-

Line 13i:

To report total deposits and refundable credits, minus advances, subtract line 13h from line 13g and enter the result on line 13i.

-

Line 14:

To report your balance due, if line 12 is more than line 13i, enter the difference on line 14.

-

Line 15:

This line calculates overpayment. If line 13i is more than line 12, subtract and enter the difference on line 15.

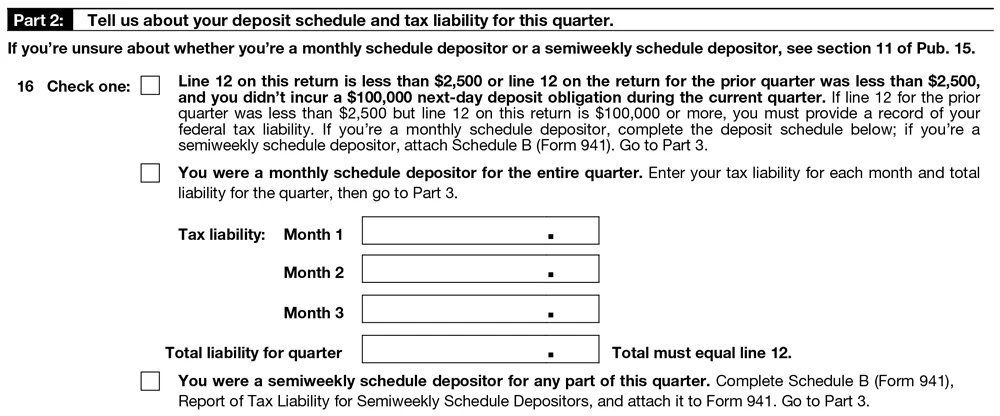

3. Part 2 - Deposit schedule and tax liability for the quarter

This part requires you to enter information about the tax liability and the time

of deposit.

-

Line 16: CheckBox

Check the appropriate box based on your tax liability. Check the boxes if it passes the following conditions.

CheckBox 1

- If the value on line 12 is less than $2500.

- If the value on line 12 was less than $2500 for the previous quarter.

- If you didn’t incur a next-day deposit obligation of $100,000 for the current quarter.

CheckBox 2

If you’re a monthly schedule depositor for the quarter. You need to enter the value of tax liability for each month during the quarter. Your total liability for the quarter should be the same as the value on line 12.

CheckBox 3

If you’re a semiweekly schedule depositor for the quarter. Enter the tax liability on Schedule B and attach it along with your Form 941.

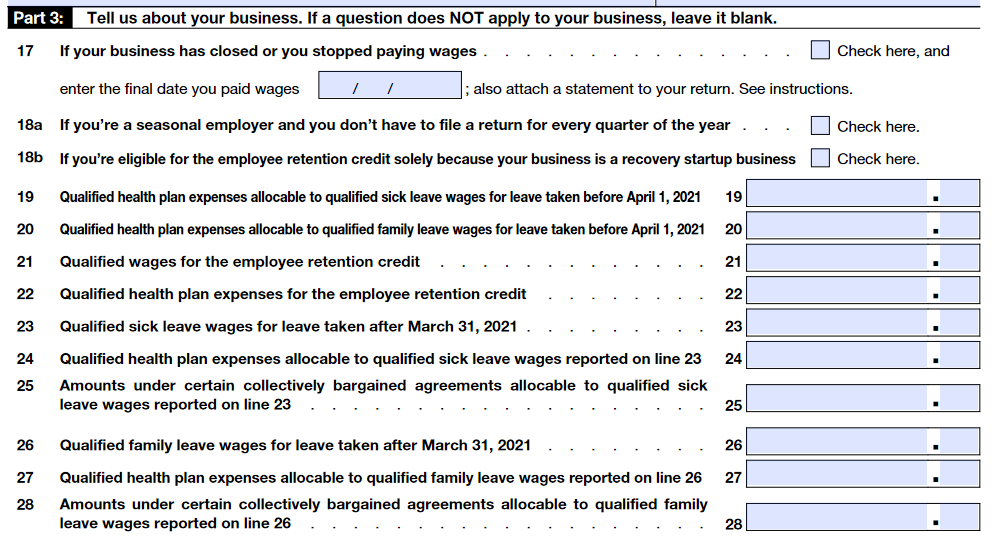

4. Part 3 - About your business

This section is used to provide information about your business.

-

Line 17: CheckBox

Check this box if your business was closed or didn’t pay any wages for the whole quarter. If you check this box, enter the date on which the wages were

finally paid. -

Line 18a:

Check this box if you’re a seasonal employer, and you aren’t required to file Form 941 for every quarter.

-

Line 18b:

Check the box on this line if your business is eligible for employee retention credit only because your business is a recovery startup business.

-

Line 19:

Enter your qualified health plan expenses allocable to qualified sick leave wages for leave taken before April 1, 2021.

-

Line 20:

Report your qualified health plan expenses allocable to qualified family leave wages for leave taken before April 1, 2021.

-

Line 21: Qualified wages for the employee retention credit (Not part of the original form. Included due to COVID-19 changes)

Enter the amount of qualified wages factored into determining the amount of the employee retention credit for which you're eligible.

-

Line 22: Qualified health plan expenses allocable to wages reported on line 21 (Not part of the original form. Included due to COVID-19 changes)

Enter the amount of qualified health plan expenses incurred for maintaining group health plan coverage for employees who were paid qualified wages that were factored into calculating the employee

retention credit. -

Line 23:

Enter any qualified sick leave wages you paid your employees for leave taken after

March 31, 2021. -

Line 24:

Report qualified health plan expenses allocable to qualified sick leave wages for leave taken after March 31, 2021.

-

Line 25:

Enter collectively bargained defined benefit pension plan contributions and collectively bargained apprenticeship program contributions allocable to qualified sick leave wages for leave taken after March 31, 2021.

-

Line 26:

Enter qualified family leave wages paid to your employees for leave taken after

March 31, 2021. -

Line 27:

Provide your qualified health plan expenses allocable to qualified family leave wages.

-

Line 28:

Use this line to report on the collectively bargained defined benefit pension plan contributions and collectively bargained apprenticeship program contributions allocable to qualified family leave wages for leave taken after March 31, 2021.

5. Part 4 - Third Party Designee - CheckBox

Check this box if you decide to discuss your Form 941 return with the IRS.

If you choose yes - Enter the designee’s name and phone number. Provide any 5 digit PIN, which should be used while talking to the IRS.

If you choose no - Skip this section.

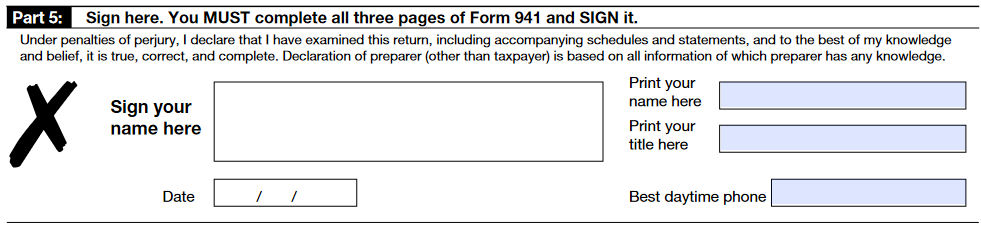

6. Part 5 - Signature

After the completion of all the parts in Form 941, you are required to sign the form before transmitting it to the IRS. Here are the signing authorities for each type of companies:

- Sole proprietorship: Individual who owns the company

- Corporation or an LLC treated as a corporation: President, vice president, or other principal officer

- Partnership or an LLC treated as a partnership: Partner, member,

or officer - Single-member LLC: Owner of the LLC or a principal officer

- Trust or estate: The fiduciary

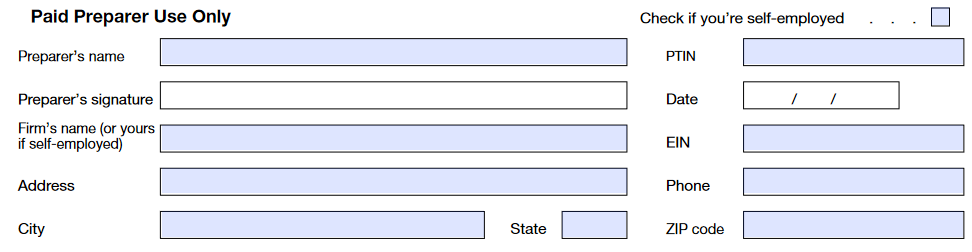

- Paid Preparers - Tax preparers must have filed a valid power of attorney form, to file Form 941 on behalf of a client. The paid preparer must provide his name, address, phone number, signature, and PTIN.

The IRS has revised Form 941 for Q2, 2021. The American Rescue Plan Act of 2021 (ARP), signed into law on March 11, 2021, includes relief for employers and their employees during COVID-19. As always employers need to report COVID-19 credits on Form 941, so the IRS has updated the form to reflect the ARP.

E-File Form 941 with ExpressEfile

Employers can e-file Form 941 easily with ExpressEfile by following a few simple steps. Just enter the required information, review the form, and transmit it directly to the IRS. The whole process takes only a few minutes.

ExpressEfile offers the lowest price of $5.95 for

filing Form 941.